En esta página

You built a strategy. The backtest curve climbs from the bottom-left to the top-right like a textbook example. You fund the account, switch it on, and a few weeks later the equity line is doing something the backtest never did: drifting sideways, then down. Nothing is broken. The code is running exactly as written. And yet the two curves — same rules, same market — have come apart.

This gap is so universal it deserves a name: the reality gap. It is the distance between what a backtest promised and what the market actually paid you. The good news is that the gap is not random bad luck — it comes from a short list of specific, well-understood causes, and once you can name them you can shrink each one.

Where the edge leaks out

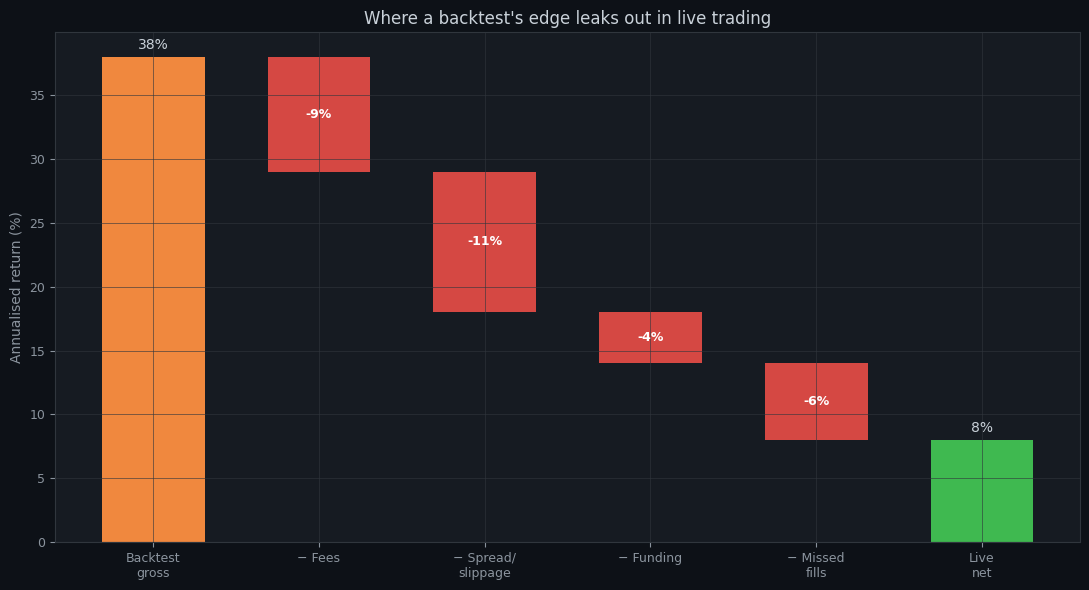

Start with the leaks that have nothing to do with whether your idea is any good. Even a genuinely profitable strategy hands back a chunk of its edge to friction the moment it goes live.

- **Fees.** A taker order on most crypto venues costs 5–10 bps each way. A strategy that turns over its capital often pays this dozens of times a month. If your edge per trade is 10 bps and your round-trip cost is 8, you have no edge.

- **Spread and slippage.** Backtests usually fill at the candle close — a price that may not have existed for any size. Live, you cross the spread, and in fast markets the price has already moved by the time your order lands.

- **Funding.** Hold a perpetual position through a funding window and you pay (or receive) the funding rate. Over a month of held positions this is a real, recurring drag a spot backtest never models.

- **Missed and partial fills.** A limit order that the backtest assumes filled may never have been hit live, so you simply miss the trade — and missing your winners while still taking your losers is its own slow bleed.

We go deeper on this in slippage and trading costs. The headline: model costs *pessimistically* in the backtest, because the live market certainly will.

The bigger problem: the edge was never there

Costs explain a haircut. They don't explain a strategy that flips from +40% to negative. For that, the usual culprit is the most seductive failure mode in all of quant trading: the edge you backtested was never real.

If you searched a big parameter space over a single slice of history and kept the combination with the best Sharpe, you didn't discover a strategy — you described that slice of history. This is overfitting, and an overfit strategy has no reason to work on data it has never seen. Live trading is, by definition, data it has never seen.

The defence is to never trust a single in-sample number. Walk-forward optimization re-fits the strategy on a rolling window and only ever judges it on the *next*, untouched window — the closest thing to live trading you can run offline. A strategy whose out-of-sample numbers hold up has earned a little of your trust. One that only looks good in-sample has earned none.

Look-ahead bias: the silent inflator

A subtler cause is look-ahead bias — letting the strategy use information it could not have had at the moment it traded. Computing a signal on the current candle's close and then "entering" at that same close. Using a daily high to decide an intraday entry. Normalising a feature using the whole dataset's mean. Each of these quietly leaks the future into the past, and each inflates the backtest by an amount you will never see live.

Look-ahead bias is insidious because it doesn't look like a bug — the backtest just looks *better*. The discipline is to make every rule answer one question: could I have known this, with certainty, at the exact moment I'm acting on it? If not, it's leakage.

The regime moved on

The last big cause is time itself. A strategy fitted on 2021's relentless bull market is a momentum bet on a world that ended. When the regime changed — rates up, leverage out, price ranging — the rules kept firing into conditions they were never tested in. Momentum doesn't crash in chop; it bleeds, slowly, while you wait for the trend that isn't coming.

This is why validation is never finished. Re-running fresh walk-forward periodically and comparing recent out-of-sample performance against the historical baseline is how you catch decay before it becomes a drawdown you can't sit through. It's also closely related to why most trading bots fail — most don't break, they quietly stop matching the market they were built for.

How to shrink the gap

You can't close the reality gap to zero, but you can shrink it from a cliff to a step:

- **Charge realistic costs in the backtest.** Use your venue's real taker fee, a conservative slippage assumption, and funding if you trade perps. If the edge survives pessimistic costs, it might survive live ones.

- **Validate out-of-sample, always.** Walk-forward or nothing. A single in-sample Sharpe is marketing, not evidence.

- **Paper trade before you fund.** [Paper trading](/blog/paper-trading-explained) on live data catches execution problems — partial fills, latency, data quirks — that no historical backtest can.

- **Size for the drawdown you'll actually live through.** Live drawdowns run deeper than backtested ones. If you can't watch a 20% drawdown without intervening, you're sized too big.

- **Expect to keep about half.** A useful prior: a well-validated strategy delivers roughly half its backtested edge live. If your strategy only works at full backtest strength, it doesn't work.

The reality gap is the price of admission to systematic trading. You pay it in returns you expected but didn't get. The traders who last are the ones who priced it in *before* they funded the account — by building backtests honest enough to disappoint them on purpose. You can do exactly that with a robustness-scored backtest that tells you how much of the edge is real before a single dollar is at risk.

Pruébalo con tus datos

Cada concepto de arriba está implementado en la plataforma. Backtest, walk-forward, paper trading, luego live — el mismo conjunto de reglas en cada etapa.