Sur cette page

Most crypto traders think they are diversified because they hold ten different coins. In a downturn they discover they were not — the ten coins fall together, in lockstep, and the portfolio behaves like one large position. For an active trader, real diversification does not come from holding more assets. It comes from running strategies that make money at different times.

Why ten coins is not diversification

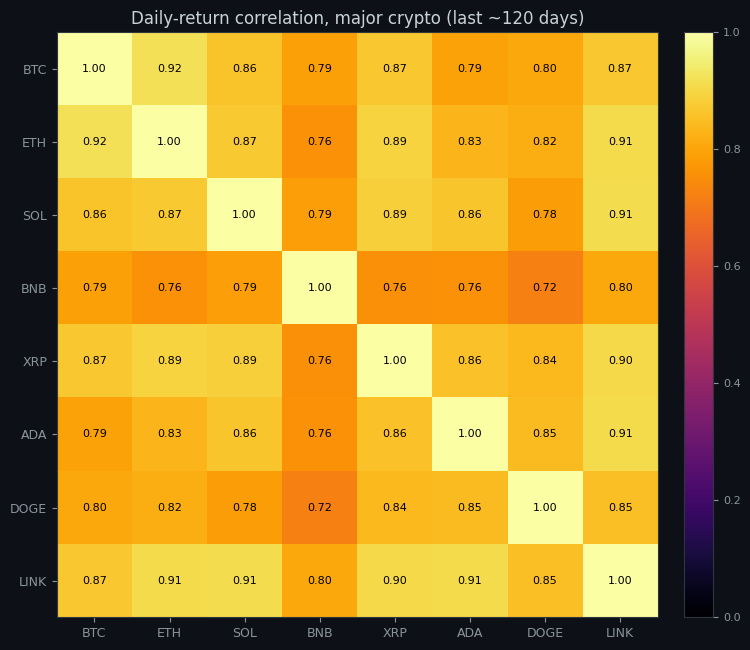

Diversification reduces risk only when the things you hold are uncorrelated — when they do not all move the same way at the same time. Crypto assets are highly correlated, especially when it matters most: in a sharp sell-off, almost everything drops together. Holding BTC, ETH, and eight altcoins gives you the feeling of spreading risk and almost none of the substance. When the tide goes out, the whole portfolio is one trade. Adding an eleventh coin does not fix this; it just adds another copy of the same bet.

The heatmap above makes the point concrete. Every pair of these eight major coins has a daily-return correlation between roughly 0.72 and 0.92 — there is not a single genuinely independent column in the grid. A portfolio of all eight is not eight bets; it is one bet on "crypto goes up", held eight times. And in the sell-off that matters, those correlations drift even closer to 1.0 — exactly when you were counting on them to be low. This is why adding coins cannot manufacture diversification: the raw material, uncorrelated return streams, simply is not there.

Diversifying strategies, not assets

The lever an algo trader can actually pull is strategy diversification. Recall that trend following profits in trending markets and mean reversion profits in ranging ones. Their returns are not just uncorrelated — over the regime cycle they are close to negatively correlated: the very conditions that hurt one tend to help the other. Run both, and when the trend strategy is grinding through a flat drawdown, the mean-reversion strategy is often in its element, and vice versa. The combined equity curve is meaningfully smoother than either component.

Where uncorrelated returns come from

- Different strategy types — trend following and mean reversion, the cleanest example, profiting in opposite regimes.

- Different timeframes — a strategy on the 4-hour chart and one on the 15-minute chart respond to different market structure and rarely draw down in sync.

- Different instruments with genuinely different behaviour — not ten correlated altcoins, but assets whose drivers actually differ.

- Different holding periods — a fast scalping strategy and a slow swing strategy experience the same market through different lenses.

How to combine strategies sensibly

Two cautions. First, check the correlation you assume — two strategies you believe are different may, on inspection, draw down together; only their actual return correlation tells the truth, so measure it rather than hoping. Second, more strategies is not automatically better. Each one you add must carry its own positive expectancy — diluting a portfolio with a mediocre strategy for the sake of a 'diversification' label just lowers the return without buying real risk reduction. Allocate capital deliberately across a small number of strategies that each stand on their own and that genuinely behave differently.

Noon Barbari supports multi-strategy portfolios with tiered position sizing — you can run several validated strategies together and backtest the combined portfolio, not just each strategy alone, so the correlation benefit (or its absence) shows up in the equity curve and drawdown. Build each strategy in the strategy designer, validate it on its own, then combine.

Diversification is not about owning more things. It is about owning things that behave differently. For a trader, that means a small set of genuinely uncorrelated strategies — and the smoother equity curve that falls out of running them together. The coins in your portfolio are the bet; the strategies you run on them are where the real diversification is decided.

Essaie-le sur tes propres données

Chaque concept ci-dessus est implémenté dans la plateforme. Backtest, walk-forward, paper trading, puis passage en live — même jeu de règles à chaque étape.