On this page

Most strategies bet on direction: will this coin go up or down? Pairs trading bets on something subtler and often more stable — the *relationship* between two coins. You go long one and short the other, so the market's overall direction cancels out, and you profit if the spread between them reverts to its normal range. It's the entry point to market-neutral, statistical-arbitrage trading, and crypto's high correlations make it surprisingly accessible.

The idea: trade the spread, hedge the market

Pick two assets that normally move together — say ETH and BTC. Their prices wander, but the *ratio* between them tends to oscillate around a stable level. When the ratio stretches unusually high, ETH is expensive relative to BTC; when it's unusually low, ETH is cheap relative to BTC. A pairs trade fades the stretch: short the expensive one, long the cheap one, and wait for the ratio to revert. Because you're long one and short the other, a broad crash or rally that hits both roughly equally barely touches you — your bet is on the spread, not the market.

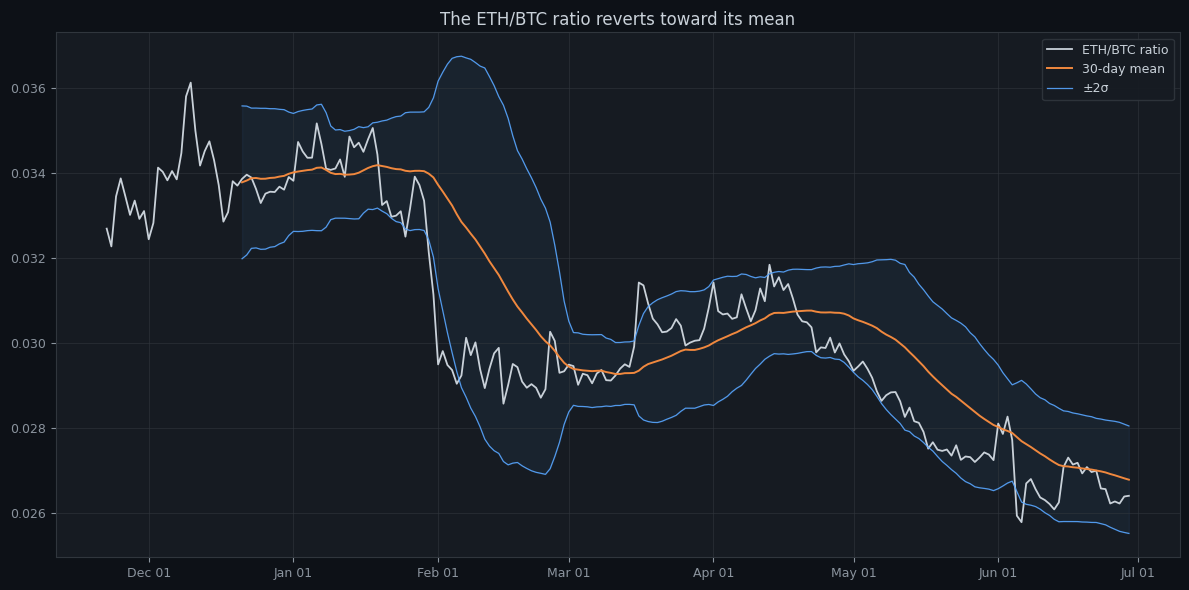

The chart is the ETH/BTC ratio with its rolling mean and ±2σ bands. The whole thesis is visible: the ratio stretches away from the mean and is pulled back, again and again. A pairs strategy enters when the ratio tags a band and exits as it returns to the mean — a mean-reversion strategy on a *spread* rather than on a single price.

The catch: correlation isn't enough

Here is where most pairs trades quietly fail. Two assets being *correlated* — moving in the same direction day to day — does not mean their ratio is *stable*. The property you actually need is cointegration: the spread between them is mean-reverting and doesn't wander off permanently. Two strongly correlated coins can still see their ratio drift to a new level and never come back, in which case your "reversion" trade just bleeds as the spread keeps widening.

How to backtest a pairs strategy

Treat the spread as your instrument. Compute the ratio (or the price-difference) series, measure how far it is from its rolling mean in standard deviations (a z-score), and define entries and exits on that z-score: enter when it exceeds ±2, exit near 0. Then test it the same way you'd test any mean-reversion strategy — across multiple regimes, net of the costs of trading *two* legs (you pay fees and spread on both sides), and with a hard stop for when the relationship simply breaks.

Watch the same risk-aware metrics as always — maximum drawdown, Sharpe — but pay special attention to the worst single trade, because a broken cointegration is where pairs strategies take their biggest losses.

Choosing the pair matters as much as the rules. The best candidates share a genuine economic link — two large layer-1s, two DeFi blue-chips, an asset and its close ecosystem token — so there's a real reason the spread should revert rather than drift to a new home. Pairs picked purely because they happened to correlate in your sample are exactly the ones most likely to decouple the moment you start trading them.

Why it's worth the effort

A genuinely market-neutral strategy is the rarest and most valuable thing in a portfolio: a return stream that doesn't care which way crypto goes. As the diversification piece argues, that's the real prize — uncorrelated returns, not more coins. A working pairs trade is one of the few honest sources of it.

In Noon Barbari you can construct the spread as a derived series and backtest z-score entries and exits on it in the strategy designer, then walk-forward to confirm the reversion held out-of-sample rather than only in the window you fitted. Pairs trading rewards the discipline of testing the relationship, not just the correlation — get that right and you've built something most traders never do.

Try it on your own data

Every concept above is implemented in the platform. Backtest, walk-forward, paper-trade, then promote to live — same rule set, all stages.